OKX, the global crypto exchange formerly operating in legal limbo in the U.S., is making a high-profile comeback. Following a $505 million settlement with the U.S. Department of Justice (DOJ), the Seychelles-based company has relaunched operations in the United States with a new centralized exchange and wallet platform tailored specifically for American users.

The firm has relocated its U.S. headquarters to San Jose, California, and tapped Wall Street veteran Roshan Robert—previously with Morgan Stanley and Barclays—to lead the U.S. expansion as CEO. The relaunch includes a phased rollout of OKX’s trading platform and wallet services for American users, with broader national access expected by the end of 2025.

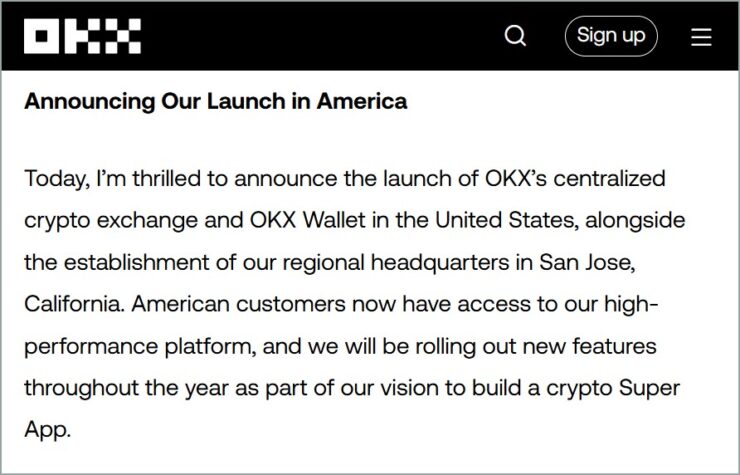

“U.S. customers now have access to our high-performance platform, and we will be rolling out new features throughout the year as part of our vision to build a crypto Super App,” said Robert in the official statement.

As part of the relaunch, users of OKCoin, a previously affiliated U.S.-facing exchange under the same corporate umbrella, will be migrated to OKX’s new infrastructure, signaling a consolidation of branding and services.

This move aligns with the growing regulatory openness under the Trump administration, which has created a more welcoming climate for crypto firms seeking U.S. legitimacy.

$505 Million Settlement Ends Legal Turmoil

OKX’s return follows the resolution of a long-running investigation by the DOJ. In February 2025, the agency disclosed that OKX—via corporate affiliate Aux Cayes FinTech Co. Ltd.—facilitated over $1 trillion in U.S. crypto transactions between 2018 and 2024 without the required money transmission licenses.

Despite public-facing policies that supposedly blocked U.S. residents, DOJ investigators found that the platform not only served U.S. customers but also helped some users bypass geographic restrictions using falsified information.

To resolve the charges, OKX agreed to:

- Pay $84 million in penalties

- Forfeit $421 million in illicit revenue

- Employ an external compliance consultant through 2027

Importantly, the DOJ confirmed that no consumer losses were reported in connection with the violations. OKX says all affected U.S. accounts have since been removed.

With regulatory penalties now behind it, OKX is working to rebuild trust through compliance. The company has pledged to strengthen internal oversight and hire independent monitors to guide its operations in the U.S.

This reset comes as OKX seeks to establish itself as a fully compliant player in a rapidly evolving U.S. crypto landscape—one where digital asset firms are increasingly integrating with traditional financial infrastructure.

Quick Facts

- OKX resumed U.S. operations after paying $505 million to settle DOJ allegations of unlicensed activity.

- The exchange processed over $1 trillion in U.S. transactions from 2018 to 2024 without proper registration.

- It has opened its U.S. headquarters in San Jose, California, and appointed Roshan Robert as U.S. CEO.

- OKX will retain external compliance oversight through 2027 as part of its agreement with federal regulators.