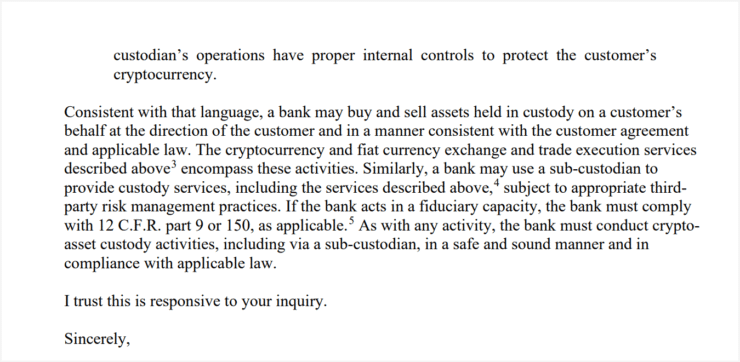

In a notable shift in federal banking policy, the U.S. Office of the Comptroller of the Currency (OCC) has reaffirmed that national banks may directly engage in cryptocurrency services on behalf of their clients—including buying, selling, and managing digital assets. The updated guidance also confirms that banks can outsource these operations to qualified third-party providers, as long as they maintain proper risk and compliance protocols.

The announcement came via a new interpretive letter issued Wednesday by Acting Comptroller Rodney E. Hood, who clarified that banks may conduct crypto-related activities at the direction of customers without needing prior regulatory approval. This move marks a significant easing of earlier constraints and aligns with broader efforts to integrate digital assets into traditional financial systems under the Trump administration’s more permissive stance.

The OCC’s policy update coincides with recent guidance from the Federal Reserve and the Federal Deposit Insurance Corporation (FDIC), suggesting a coordinated shift toward regulatory normalization of digital assets within the U.S. financial framework.

OCC Expands Crypto Permissions as Agencies Reverse “Choke Point”-Era Barriers

This latest directive from the OCC builds on a larger regulatory transformation that is quietly dismantling the restrictive policies that once defined the federal approach to crypto. Just two weeks ago, both the Fed and FDIC rescinded requirements for banks to obtain prior approval before engaging with digital asset services—effectively bringing an end to practices often described as “Operation Choke Point 2.0.”

The OCC’s current stance reinstates the openness seen in 2020 under Interpretive Letter 1170, which originally authorized national banks to provide crypto custody services. That earlier guidance had characterized digital asset management—including the safeguarding of private cryptographic keys—as a natural evolution of traditional banking. However, those allowances were subsequently scaled back amid tighter federal scrutiny.

With the new interpretive letter now in force, national banks regain the authority to offer crypto-related services and partner with external vendors—without additional bureaucratic steps. The timing is critical, as many financial institutions are exploring digital assets but lack the infrastructure or capacity to do so in-house.

The update also comes as public figures, including Eric Trump, continue to criticize legacy banking institutions for lagging behind in technology and innovation. The OCC’s greenlight may now empower banks to compete more directly with crypto-native platforms.

OCC’s Crypto Greenlight Builds on Broader Regulatory Momentum

The OCC’s guidance is part of a wider regulatory recalibration. In March, the agency released Interpretive Letter 1183, which reaffirmed that crypto custody, distributed ledger technology (DLT), and stablecoin activities are permissible for national banks, provided they implement robust risk management frameworks.

By categorizing these services as legitimate “crypto-asset activities,” the OCC signaled that innovation is not only allowed but encouraged—so long as it’s balanced with supervisory oversight. The announcement was swiftly mirrored by the FDIC. Later that same month, Acting Chairman Travis Hill declared the agency was “turning the page” on what he described as an overly cautious and flawed crypto policy approach.

Together, these moves from the OCC and FDIC reflect a decisive pivot from the regulatory drag that has long slowed institutional adoption of digital assets. The message is now unmistakable: traditional banks are welcome to participate in the crypto economy—as long as they remain accountable and compliant.

Quick Facts

- Regulatory Shift: The OCC now permits national banks to offer crypto custody and trading services on behalf of clients.

- Outsourcing Allowed: Banks can outsource these services to third-party providers, provided proper risk controls are in place.

- Policy Reversal: The new guidance eliminates previous requirements for prior regulatory approval to engage in crypto activities.

- Industry Impact: The decision opens the door for deeper integration of cryptocurrencies into mainstream banking services.