Quick Facts:

- Fed Chair Jerome Powell acknowledged concerns over crypto debanking, stating it needs further review.

- Republican lawmakers have accused U.S. regulators of discouraging banks from servicing crypto firms, likening it to Operation Choke Point.

- The Trump administration has signaled a shift in policy, working to reverse restrictive measures imposed during the Biden era.

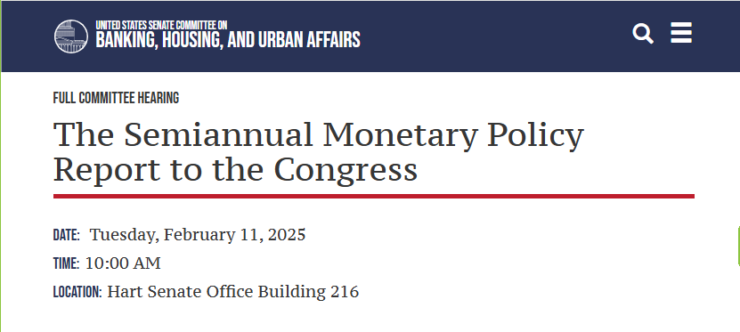

Federal Reserve Chair Jerome Powell has weighed in on the ongoing debanking controversy, acknowledging concerns that crypto firms and other industries have been unfairly cut off from banking services. Speaking before the Senate Banking Committee on Tuesday, Powell stated that the issue of debanking needs to be reassessed, given its impact on financial markets and innovation.

“I will tell you that I am struck, and my colleagues and I are struck by the growing number of cases of what appears to be debanking and we’re determined to take a fresh look at that,” Powell said.

Powell’s comments follow months of tension between crypto firms and traditional banking institutions, with several reports suggesting that U.S. regulators discouraged banks from servicing crypto companies under the Biden administration. The issue gained renewed political traction after Republican lawmakers accused financial watchdogs of leveraging regulatory pressure to limit crypto’s access to the banking sector—a practice likened to the controversial “Operation Choke Point” that targeted certain industries under the Obama administration.

Regulatory Realignment Under Trump Administration

Since Donald Trump’s return to the White House, his administration has rapidly moved to reverse restrictive financial policies from the previous government, including those impacting crypto banking access. The ongoing regulatory overhaul aims to eliminate what Republican lawmakers call “Operation Choke Point 2.0”.

Federal Reserve Chair Jerome Powell’s recent remarks align with this shift, as Trump-appointed financial watchdogs reevaluate the role of the Fed, the FDIC, and the OCC in restricting banking access for crypto firms. The administration’s efforts include the formation of the White House Crypto Council, a reassessment of banking policies impacting digital assets, and the downsizing of the SEC’s crypto enforcement unit.

During the Senate Banking Committee hearing, Powell thanked Senator Cynthia Lummis for highlighting a controversial Fed policy that directed greater supervisory scrutiny on bankers linked to sensitive activities and speech. Powell acknowledged the removal of a Federal Reserve policy that heightened scrutiny on banks dealing with politically sensitive clients, a move praised by Senator Cynthia Lummis.

Stablecoin Regulation and CBDC

While crypto oversight wasn’t a central topic at Powell’s Senate hearing, key issues like stablecoin regulation and central bank digital currencies (CBDCs) were brought into focus. Powell reaffirmed the Federal Reserve’s support for stablecoin regulations, acknowledging their growing role in financial markets and the need for a clear legal framework to govern their use.

However, the discussion took a firm stance against CBDCs, with Powell delivering an unequivocal response when asked whether he would commit to never launching a digital dollar. His simple response: “Yes.”

This position aligns with the broader anti-CBDC sentiment under the Trump administration, which has outright rejected China and Europe’s approach of rolling out digital fiat currencies. With Republican majorities in Congress and Trump’s pro-crypto stance, the likelihood of a U.S. government-backed digital dollar has all but disappeared.

Powell is set to speak again at a House of Representatives hearing on Wednesday, where lawmakers are expected to further probe the Fed’s position on stablecoins, banking regulations, and crypto industry policies