Binance is forcefully contesting a $1.76 billion lawsuit filed by the FTX estate, asking a Delaware bankruptcy court to dismiss the case on the grounds that it is “legally deficient” and misdirected. In a motion filed last week, Binance argued that the lawsuit attempts to rewrite the narrative of FTX’s collapse by blaming outside parties instead of its founder, Sam Bankman-Fried.

The legal dispute centers on a July 2021 share repurchase agreement in which FTX bought back Binance’s equity stake. The FTX estate claims the transaction was financed using misappropriated customer funds and is seeking to recover the payment through bankruptcy clawback provisions.

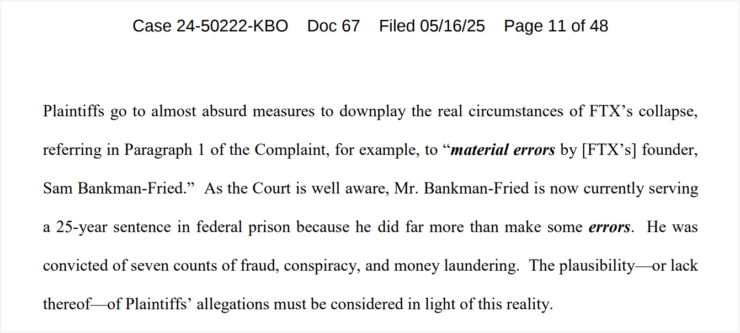

Binance rejected the allegations, describing the lawsuit as an effort to “shift responsibility” away from the true cause of FTX’s failure—a massive internal fraud orchestrated by Bankman-Fried, who is now serving a 25-year prison sentence for wire fraud and conspiracy.

“The plaintiffs are pretending FTX didn’t collapse due to one of the largest corporate frauds in history,” Binance said in the filing.

The exchange maintains that neither it nor its former CEO, Changpeng “CZ” Zhao, had any role in FTX’s financial misconduct and argues that the clawback claims lack legal standing.

Binance Defends Buyback Deal and Challenges FTX’s Insolvency Claims

At the heart of the lawsuit is a 2021 transaction in which FTX repurchased a 20% equity stake from Binance—originally acquired in 2019—using a mix of BNB, BUSD, and FTT tokens. FTX’s bankruptcy administrators allege that the firm was already insolvent at the time of the deal and that the repurchase was funded using customer deposits.

Binance disputed the insolvency claim, noting that FTX continued operating for more than a year after the transaction. The exchange argues that if FTX had truly been insolvent at the time, it could not have sustained operations or concealed financial distress for such a prolonged period.

The lawsuit also accuses Zhao of triggering a market panic that contributed to FTX’s collapse, citing a November 6, 2022 tweet in which he announced Binance would liquidate its FTT holdings “due to recent revelations.” The tweet came shortly after CoinDesk reported on troubling financial links between Alameda Research and FTX.

Binance defended Zhao’s statement as a reaction to public information and denied any intent to sabotage a competitor. “The complaint offers no evidence that Zhao’s statements were false,” the filing said, adding that the legal arguments fail to establish intent or direct causation.

Binance Questions Jurisdiction and Legal Standing of Case

Binance’s motion to dismiss also challenges the U.S. court’s jurisdiction over the case. The company argues that none of the involved entities are based in the United States and that the disputed transactions did not occur within U.S. borders.

This jurisdictional challenge is part of a broader defense against several clawback lawsuits brought by the FTX recovery team, which has been aggressively pursuing claims to recover funds for creditors following FTX’s collapse in late 2022. That failure left billions in customer assets unaccounted for and triggered a broader crisis of confidence in the crypto industry.

While the court has yet to rule on Binance’s motion, the outcome could influence how bankruptcy-related clawbacks are applied to international transactions and non-U.S. entities in crypto insolvency cases going forward.

Quick Facts

- Binance has filed a motion to dismiss FTX’s $1.76 billion lawsuit, calling it legally baseless and an attempt to shift blame from Sam Bankman-Fried.

- The case revolves around a 2021 share buyback in which FTX repurchased Binance’s equity using BNB, BUSD, and FTT—allegedly with misused customer funds.

- Binance disputes FTX’s insolvency claims and denies that former CEO CZ’s tweet triggered the collapse, calling the lawsuit speculative and unfounded.

- Binance is also contesting the U.S. court’s jurisdiction, noting that none of the involved parties are based in the United States or conducted the transaction domestically.