The U.S. Securities and Exchange Commission (SEC) has officially declared that protocol-level staking—when linked directly to a blockchain’s consensus mechanism—does not constitute a securities transaction under U.S. law.

The announcement, released Thursday, marks one of the most significant updates to crypto policy under the current SEC leadership. It affirms that crypto assets staked to secure decentralized, permissionless networks are not being “offered or sold” as securities under the Securities Act of 1933 or the Securities Exchange Act of 1934—so long as they are not packaged or promoted by third parties.

This includes tokens used in proof-of-stake consensus models to validate transactions and earn rewards within network-defined rules, without profit guarantees from intermediaries. The clarification represents a major departure from the aggressive stance of former SEC Chair Gary Gensler, who argued that many staking activities fell squarely under securities regulation.

Under the new administration, this guidance may signal a lasting change in how U.S. regulators differentiate decentralized infrastructure from investment contracts, a debate that has long shaped crypto regulation.

SEC Defines Boundaries—But Leaves Some Staking Models Unclear

While the updated guidance brings long-awaited clarity to certain types of staking, it stops short of resolving regulatory ambiguity around more advanced and composable staking mechanisms—especially liquid staking and restaking.

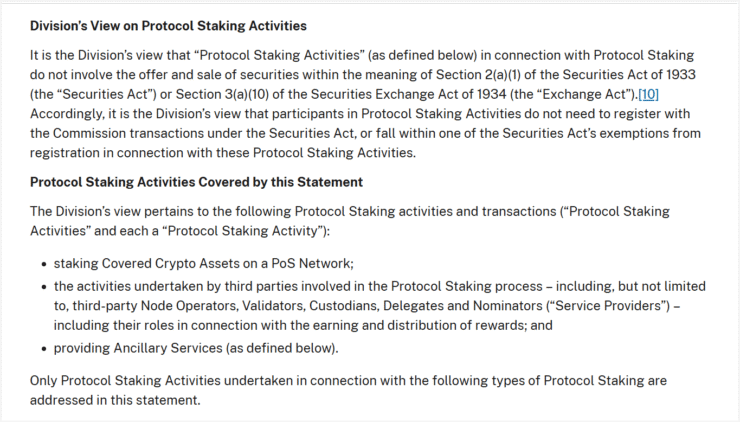

According to the SEC, the following are not considered securities offerings when conducted within decentralized network structures:

- Self-staking: Users stake their own tokens directly into the network.

- Self-custodial delegation: Users delegate to validators without surrendering asset ownership.

- Custodial staking: Service providers stake on behalf of users without offering guaranteed profits or shifting control of the underlying assets.

The update emphasizes that these models do not involve a third party promising returns, a critical factor under the Howey Test, the legal standard for defining securities.

However, the SEC withheld judgment on liquid staking and restaking, two rapidly evolving practices that allow staked assets to be reused in DeFi or re-delegated across multiple platforms. These models, the agency noted, could still fall under securities rules depending on how they are marketed and structured.

Importantly, this release reflects staff-level guidance, not formal rulemaking. While not legally binding, it sets the tone for future enforcement and provides stakeholders with much-needed direction after years of uncertainty.

SEC Commissioner Blasts Policy Shift as ‘Legally Flawed’

Not everyone at the SEC agrees with the new direction. Commissioner Caroline Crenshaw issued a strong dissent, criticizing the guidance as legally inconsistent and politically motivated.

Crenshaw referenced previous enforcement actions—including those against Coinbase and Kraken—where courts found elements of staking-as-a-service models to fall under securities law. She also cited the same-day dismissal of the Binance lawsuit as a troubling signal that the agency is pivoting from established positions without clear justification.

“Rather than promote clarity, this approach continues to sow uncertainty around what the law is and what parts of it the Commission is willing to enforce,” she wrote.

Crenshaw accused the agency of adopting a “‘fake it till we make it’ approach to crypto,” warning that it may undermine the SEC’s credibility and complicate future legal proceedings. Her dissent highlights the deepening ideological divide within the agency as it navigates the evolving crypto landscape under political and market pressure.

Quick Facts

- The SEC has clarified that protocol-level staking tied to network consensus is not a securities transaction.

- The guidance applies to self-staking, self-custodial delegation, and custodial staking—if no third party guarantees profit.

- The SEC did not clarify the status of liquid staking or restaking, leaving them in regulatory limbo.

- The update reflects staff interpretation, not legally binding rulemaking.

- SEC Commissioner Caroline Crenshaw strongly opposed the move, calling it legally flawed and dangerous to agency credibility.