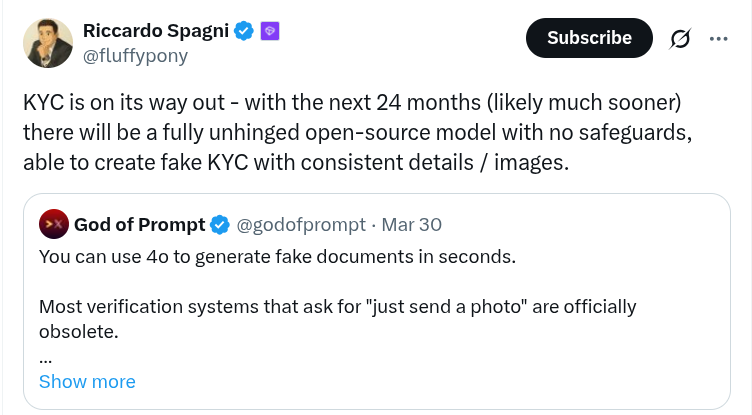

Mandatory identity verification may soon be rendered ineffective by artificial intelligence, according to Monero’s former lead maintainer Ricardo Spagni. Posting under the handle @fluffypony, Spagni warned that current Know Your Customer (KYC) protocols are on track to become obsolete within two years.

Spagni’s post on X projected a future where AI-generated identities bypass verification systems that rely on user-submitted photos and documents. He stated that “within the next 24 months (likely much sooner)” open-source models will exist “with no safeguards,” capable of producing entirely fake yet cohesive KYC documentation. He included AI-generated images showing fabricated individuals holding forged identification documents.

“It’s not perfect, and weirdly inconsistent – but it’s getting there!” Spagni added.

AI-Created Fakes Threaten Current Standards

Spagni’s comments were triggered by a post from another user, Good of prompt, who demonstrated how GPT-4o tools can now produce convincing fake documents in seconds. That post included seven examples of AI-generated IDs, noting that verification systems that only request a photo are now “officially obsolete.”

Spagni amplified the warning by showcasing how AI can generate not just random faces, but entire synthetic personas, complete with realistic ID cards. The implication: AI-generated KYC forgeries may soon be indistinguishable from legitimate submissions, overwhelming systems that rely on manual review or basic image analysis.

As the former maintainer of the privacy-focused cryptocurrency Monero, Spagni’s comments carry weight within the digital asset space. Known for opposing centralized surveillance and promoting anonymous transactions, Spagni has long criticized KYC requirements as vulnerable and ineffective. His latest warning places AI at the center of that vulnerability.

By referencing “fully unhinged” AI models with “no safeguards,” Spagni indicated concern not just about the technology’s capabilities, but also about its accessibility. Open-source development ensures that once such tools are released, they can spread widely with no regulatory oversight or constraints.

The examples shared by both Good of prompt and Spagni highlight a growing technological gap between regulatory compliance demands and available evasion tools. If AI can generate documentation accurate enough to fool KYC systems, platforms may soon be forced to adopt advanced forensic or biometric verification methods.

The prospect of publicly available models generating realistic KYC forgeries raises questions for banks, exchanges, and regulators worldwide. As Spagni noted, the inconsistencies in today’s fakes are narrowing—suggesting a future where machine-generated identities routinely pass for real ones.