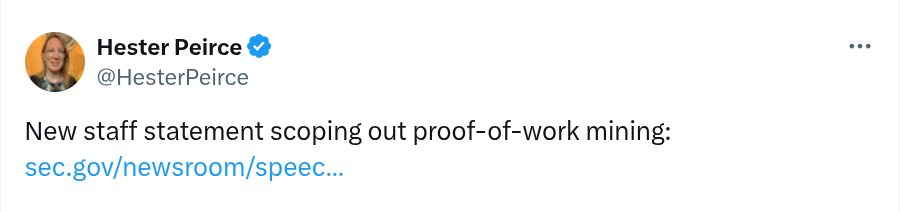

The U.S. Securities and Exchange Commission (SEC) has confirmed that proof-of-work (PoW) mining does not constitute securities dealing under federal law, providing long-awaited clarity for the cryptocurrency industry. The SEC’s Division of Corporation Finance issued a statement on March 20 outlining its position on “Protocol Mining” activities, stating that miners who validate transactions on public, permissionless PoW networks are not engaged in securities transactions.

The SEC’s analysis applies to “Covered Crypto Assets” that are essential to the operation of a decentralized network. The agency stated that these assets, when mined through PoW, do not meet the definition of a security under the Securities Act of 1933 and the Securities Exchange Act of 1934.

The statement emphasized that solo miners and mining pools, which contribute computational resources to validate transactions and secure the network, do not engage in investment contracts as defined by the Howey Test.

Clarifying the Legal Status of Mining

The SEC’s determination hinges on a fundamental distinction: PoW miners are compensated for providing a service rather than investing in an enterprise managed by others.

The agency explained that miners earn rewards directly from the network’s protocol for verifying transactions and securing the blockchain. Because the miner’s compensation is generated through their own computational efforts rather than from the managerial actions of a third party, the SEC ruled that PoW mining does not constitute an investment contract.

“In evaluating the economic realities of a transaction, the test is whether there is an investment of money in an enterprise premised on a reasonable expectation of profits to be derived from the entrepreneurial or managerial efforts of others,”

the SEC stated.

“A miner’s expectation to receive Rewards is not derived from any third party’s managerial or entrepreneurial efforts upon which the network’s success depends.”

The agency made it clear that PoW networks operate through a decentralized system of independent participants, further supporting its view that mining does not fit the legal framework for securities regulation.

The statement also reaffirmed that mining pools, which allow multiple participants to combine computational power, are not securities offerings, as individual miners still contribute their own resources and are not dependent on managerial oversight.

Impact on Cryptocurrency Regulation

While the SEC did not name specific blockchains, the ruling has direct implications for Bitcoin, Dogecoin, Litecoin, and Monero, all of which operate on PoW consensus mechanisms. The decision aligns with the Commodity Futures Trading Commission’s long-standing classification of Bitcoin as a commodity rather than a security.

The SEC’s announcement arrives amid shifting U.S. policy toward digital assets. President Donald Trump has signaled a pro-crypto stance, with plans to establish the Council of Advisers on Digital Assets to create regulatory clarity.

The Blockchain Association has also indicated that a cryptocurrency market structure bill is expected by summer. Kristin Smith, the association’s CEO, suggested that lawmakers are working to finalize the bill by August.

The SEC’s statement is expected to provide much-needed regulatory certainty for PoW miners and crypto investors. By distinguishing mining rewards from securities transactions, the agency has removed a major legal ambiguity that could have led to enforcement actions against blockchain participants.

1

1